Student Loan Debt affects over 43 million Americans, shaping how they live, work, and plan their futures. For many, repayment becomes a long-term struggle that delays major life milestones like buying a home or saving for retirement.

This debt includes federal and private loans. Federal loans come from the government and often include repayment flexibility or forgiveness programs. Private loans, issued by banks or other lenders, usually carry higher interest rates and fewer protections.

Across the nation, total Student Loan Debt now exceeds $1.7 trillion, second only to mortgage debt. That figure shows how deeply education costs burden the U.S. workforce. Each graduating class enters adulthood already owing thousands.

This growing crisis deserves urgent attention. Rising tuition and stagnant wages create a chain of dependency that traps many borrowers. Breaking that chain begins with understanding how student debt truly shapes American life.

How Student Loan Debt Affects Everyday Life

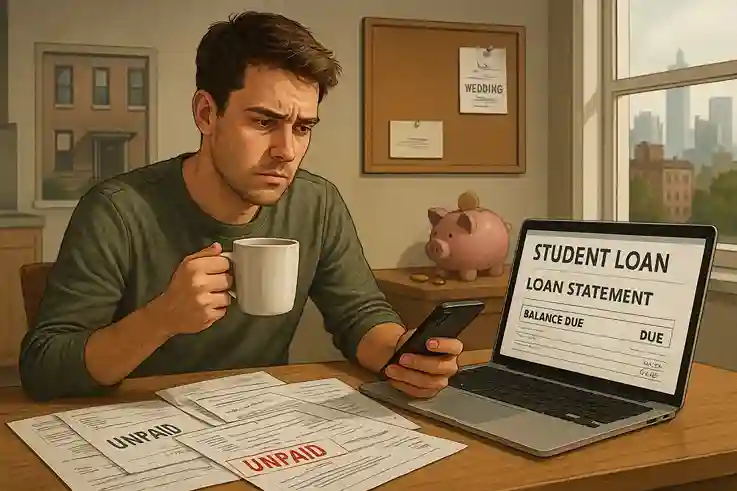

Student Loan Debt reaches far beyond monthly payments. It creates emotional stress that lingers through daily life. Many borrowers feel constant pressure as interest grows faster than their income. That tension builds anxiety, making financial decisions heavier and more complex.

The financial weight of this debt reshapes major life goals. Homeownership gets delayed because down payments feel out of reach. Marriage and family planning often wait until loans shrink or stabilize. Savings goals fall behind, leaving retirement plans uncertain. Each missed milestone connects back to the same source—income tied too tightly to repayment demands.

This dependency traps borrowers in a cycle. When income increases slightly, higher living costs or interest still limit progress. The result feels like running uphill without gaining ground. Borrowers work harder, yet freedom seems distant. Understanding this emotional and financial web is essential before exploring why Student Loan Debt keeps expanding nationwide.

“Every payment you make is a step closer to freedom from debt.”

The Truth Behind the Growing Student Loan Crisis

Student Loan Debt rises year after year, tightening its hold on millions of Americans. The growth is no accident. It results from connected causes—rising tuition, compounding interest, and stagnant wages. Each factor depends on the other, forming a system that keeps borrowers locked in repayment for decades.

Tuition Rises, Students Owe Mor

College costs increase each decade, so students must borrow more to cover tuition. For instance, average tuition at public universities has tripled since the 1990s, surpassing both inflation and wage growth. As a result, a degree that once symbolized opportunity now feels like a toll gate that few can afford. Families stretch savings, take on second jobs, or rely heavily on loans just to access higher education.

In this scenario, the dependency chain becomes clear: higher tuition → higher borrowing → higher debt load. Each year, this cycle repeats, pushing the chain forward. Students depend on loans to start school, while colleges depend on that borrowed money to fund operations and programs. Consequently, this loop perpetuates the student loan crisis, making it increasingly difficult for borrowers to achieve financial freedom.

Interest Grows While Wages Stall

After graduation, repayment begins, but income growth rarely keeps pace with rising debt. For example, the average borrower owes around $37,000 and often faces interest rates between 4% and 7%. Over time, even consistent payments can feel ineffective as interest accumulates faster than balances decrease.

Borrowers earn money, yet they owe more. They make payments, but progress often appears minimal. In this case, the dependency—income flowing directly into interest—traps many for years. Moreover, slow wage growth intensifies the problem, transforming what should be short-term loans into long-term financial burdens.

A System Built on Dependency, Not Freedom

The truth behind the student loan crisis lies in its structure. For instance, students owe more because colleges continually raise tuition. Meanwhile, they struggle as wages grow slower than debt, and they remain trapped because interest keeps accumulating. Consequently, each link reinforces the next, keeping borrowers dependent on repayment rather than moving toward financial freedom.

However, breaking free begins with understanding these connections. Once borrowers recognize how tuition, wages, and interest interact, they can adopt smarter strategies—such as refinancing, income-driven repayment plans, or targeted forgiveness programs. Ultimately, understanding these structures opens the path to real solutions and lasting relief from Student Loan Debt.

Federal vs. Private Student Loans: Know the Difference

Understanding the difference between federal and private loans is essential for managing Student Loan Debt effectively. Each loan type depends on distinct systems, rules, and repayment options. The way they function determines how easily borrowers can move toward financial stability.

Federal Loans: Government Support with Flexibility

Federal loans operate under government programs designed to make education more accessible. Specifically, the Department of Education controls terms, interest rates, and repayment options. Rates are fixed, which means they stay the same throughout repayment. Eligibility depends on financial need, school enrollment, and U.S. citizenship.

Borrowers benefit from built-in flexibility. Federal loans offer multiple repayment plans, including income-driven options where monthly payments depend on income and family size. Additionally, some borrowers qualify for loan forgiveness programs after years of consistent payment, especially in public service or teaching roles. In dependency terms, lower income leads to smaller payments; steady payments lead to forgiveness. This chain supports stability and encourages responsible repayment behavior.

Another crucial feature is deferment and forbearance. When financial hardship strikes, borrowers can pause payments temporarily without defaulting. As a result, that safety net reduces emotional stress and keeps loans manageable during difficult times.

Private Loans: Lender Control with Higher Risk

Private loans operate differently. Specifically, banks, credit unions, and other financial institutions control interest rates, approval terms, and repayment structures. Rates can be variable, which means they rise or fall with market changes. Eligibility depends more on credit score and co-signer reliability than on financial need.

Private loans rarely offer forgiveness or flexible repayment. As a result, borrowers face fewer protections if income drops or emergencies arise. Interest accrues during school and grace periods, increasing total costs. Here the dependency shifts—higher rates cause faster balance growth; limited options cause repayment strain. Consequently, the result often traps borrowers in stricter financial obligations.

Choosing the Right Path Forward

Understanding how these two systems differ reveals why many Americans struggle with Student Loan Debt. While federal loans offer structure and protection, private loans demand caution and consistent income. Additionally, each borrower’s situation depends on their career path, earning potential, and risk tolerance.

Understanding this structure builds the foundation for solutions. The next step is learning how to break free through smart strategies—refinancing, forgiveness, and disciplined repayment—to finally loosen the hold of student debt.

Comparison Table: Federal vs. Private Student Loans

| Aspect | Federal Student Loans | Private Student Loans |

|---|---|---|

| Lender | U.S. Department of Education | Banks, credit unions, or private lenders |

| Interest Rates | Fixed and generally lower | Variable or fixed, often higher |

| Eligibility | Based on financial need, enrollment, and citizenship | Based on credit score, income, and co-signer |

| Repayment Options | Multiple plans including income-driven repayment | Limited or fixed repayment structures |

| Forgiveness Programs | Available (Public Service Loan Forgiveness, Teacher Forgiveness) | Rare or unavailable |

| Deferment/Forbearance | Offered during hardship or unemployment | Limited or at lender’s discretion |

| Credit Check Requirement | Not required for most loans | Required, often with co-signer |

| Subsidized Options | Yes, government pays interest while in school | No, interest accrues immediately |

| Loan Servicer Control | Federal rules and borrower protections | Lender controls terms and policies |

| Typical Dependency | Lower income → smaller payments → possible forgiveness | Higher rate → faster interest growth → longer repayment |

Strategies to Break Free from Student Loan Debt

Escaping Student Loan Debt begins with smart, practical steps. Each decision depends on another, forming a chain that either slows or accelerates financial freedom. By changing one link—interest, payment size, or plan structure—you shift the entire outcome toward relief.

Refinancing for Lower Interest

Refinancing replaces old loans with a new one at a lower rate. As a result, lower interest means a smaller total cost, and a smaller cost means faster repayment. This dependency—reduced rate → reduced burden → reduced time—creates measurable progress. However, refinancing federal loans into private ones removes protections, so borrowers should calculate carefully before switching.

Income-Driven Repayment Plans

Federal income-driven plans adjust payments based on earnings. As a result, lower income results in smaller payments, keeping accounts in good standing even during hardship. Then, after consistent repayment, remaining balances may qualify for forgiveness. Overall, this structure builds stability, linking steady effort to long-term relief.

Forgiveness Programs

Programs like Public Service Loan Forgiveness reward borrowers who work in government or nonprofit jobs. In this case, the dependency chain is clear: service leads to eligibility; eligibility leads to cancellation. Consequently, each payment brings borrowers closer to freedom, not just progress on paper.

Extra Payments Toward Principal

Adding even small extra payments each month targets the principal directly. As the principal decreases, interest accumulation slows, which creates a ripple effect that speeds payoff. In this way, the sequence—extra payment → smaller balance → faster freedom—turns consistent effort into real results.

Consolidation for Simplicity

Combining multiple loans into one simplifies management. One monthly payment reduces confusion and missed deadlines. Simplicity encourages consistency, and consistency strengthens discipline.

Every action builds on the one before it. Refinancing lowers costs, income-driven plans stabilize payments, forgiveness clears balances, and extra payments accelerate results. These strategies work best together, not alone.

Smart Budgeting and Mindset Shifts That Support Freedom

Breaking free from Student Loan Debt requires more than financial strategies—it demands a mindset that supports action. Budgeting and belief work together, each depending on the other. Smart planning controls money flow, while positive thinking controls motivation.

Create a Clear, Goal-Linked Budget

Start with a detailed budget that maps income, expenses, and repayment goals. Then, track every dollar to reveal spending patterns. Use the dependency: awareness → control → improvement. When borrowers see where money goes, they can redirect small amounts toward debt payments. For example, even $50 extra per month can shorten repayment by years. Next, prioritize essentials, automate savings, and limit discretionary costs without removing joy completely. Ultimately, a budget succeeds when it fits life, rather than restricting it.

Use the 50/30/20 Framework

Divide income approximately as 50% for needs, 30% for wants, and 20% for debt and savings. This approach creates financial balance. If income fluctuates, adjust the percentages while maintaining consistent debt repayment. Maintaining this routine reinforces discipline and supports steady progress over time.

Adopt the Temporary Debt Mindset

See debt as a temporary challenge, not a permanent burden. Instead of thinking, “I’ll never be free,” adopt the mindset, “I’m reducing what I owe each month.” This shift eases stress and encourages consistent action. The chain is clear: strong mindset → steady habits → measurable progress. Borrowers who believe in eventual freedom take action sooner and maintain consistency over time.

Build Habits That Reinforce Progress

Even minor choices can produce compounding results. For example, bringing lunch from home, postponing big purchases, or applying tax refunds toward payments all gradually lower long-term costs. Consequently, each decision moves borrowers closer to financial freedom. Over time, these small wins build momentum, transforming anxiety into confidence and control.

Expert Insights: on Student Loan Debt

The Importance of Planning

Financial advisors stress that careful planning is essential for escaping Student Loan Debt. For example, experts suggest starting with a clear repayment strategy, tracking spending, and exploring all federal repayment and forgiveness options before considering private alternatives. According to the U.S. Department of Education, income-driven repayment plans and loan forgiveness programs can reduce financial strain when used correctly.

Understanding the Dependency Chain

In this context, the dependency chain is clear: better planning → better repayment outcomes → faster debt freedom. Consistent payments, informed decisions, and active monitoring reinforce one another. Borrowers who adjust strategies as needed often reduce total interest paid and shorten repayment timelines.

Consulting Certified Professionals

Additionally, certified financial professionals can help evaluate refinancing, manage multiple loans, and select repayment plans tailored to individual situations. Consulting a qualified advisor helps borrowers avoid costly mistakes and stay on track toward financial freedom.

Ultimately, following expert guidance and leveraging government resources links structured planning to long-term independence. Consequently, student loan freedom becomes achievable through consistent effort, informed choices, and sustainable financial habits.

👉 Federal Student Aid – U.S. Department of Education

Building a Life Beyond Student Loan Debt

Lessons Learned and Key Takeaways

Escaping Student Loan Debt begins with awareness and strategy. By understanding how loans work, borrowers can identify the most effective repayment options. Federal versus private loans, income-driven plans, refinancing opportunities, and forgiveness programs all create choices that, when used wisely, shorten repayment timelines. Moreover, budgeting and mindset shifts reinforce these financial strategies. Tracking spending, automating payments, and treating debt as a temporary challenge help borrowers maintain consistency and avoid setbacks. Each lesson emphasizes the dependency chain: informed choices lead to better planning, better planning leads to disciplined action, and disciplined action leads to financial progress.

Breaking the Cycle Through Awareness and Strategy

In this context, awareness alone is not enough. Borrowers must combine knowledge with action to break the cycle of debt dependence. Applying small, consistent changes—like allocating extra funds to principal, adjusting budgets, or participating in forgiveness programs—gradually reduces balances. Consequently, what once felt like an overwhelming burden becomes manageable. This approach proves that even long-term debt can be tackled systematically when each decision is intentional and interconnected.

Building a Supportive Community

Additionally, sharing experiences strengthens the journey. Borrowers who discuss challenges, strategies, and successes in forums, social media groups, or comments sections create a network of accountability and encouragement. For example, exchanging tips on budgeting or repayment schedules can inspire others to take proactive steps. Community involvement reinforces positive habits and keeps borrowers motivated, ensuring that the path toward debt freedom feels less isolating.

Achieving Long-Term Financial Independence

Ultimately, financial freedom begins when borrowers control their debt instead of letting it control them. Each repayment, adjustment, or informed decision contributes to long-term independence. Therefore, staying disciplined, seeking expert guidance when needed, and consistently applying effective strategies make the difference between ongoing debt and true liberation. Every action counts, and over time, consistent effort compounds into real results.

By following these lessons, combining awareness with strategic action, and participating in a supportive community, borrowers can envision a life beyond Student Loan Debt—one where financial choices create freedom, stability, and lasting peace of mind.

FAQ – Student Loan Debt

Conclusion

Escaping Student Loan Debt is challenging but achievable with awareness, strategy, and consistent action. By understanding how loans work, comparing federal and private options, and applying repayment strategies like refinancing, income-driven plans, and forgiveness programs, borrowers can regain control over their finances.

Moreover, building smart budgeting habits and adopting a mindset that treats debt as temporary helps maintain steady progress. Small, consistent actions—extra payments, tracking spending, or using refunds strategically—compound over time, turning manageable steps into significant results.

Ultimately, the key is to see debt not as a permanent burden but as a challenge to overcome. By combining knowledge, discipline, and expert guidance, borrowers can break free from the cycle of debt and move toward long-term financial independence. Finally, sharing experiences, asking questions, and learning from others strengthens the journey. Every choice and action matters. True financial freedom begins when you control your debt, rather than letting it control you.

Have you faced challenges with student loans or found creative ways to stay debt-free?

Share your story in the comments. Let’s build a smarter, stronger future together—one borrower at a time.

Michael Reyes is a versatile blogger with a primary focus on farming and sustainable living. Growing up close to nature, he developed a deep interest in agriculture and enjoys sharing practical tips on backyard farming, modern cultivation techniques, and eco-friendly practices. While farming remains his specialty, Michael also writes on a wide range of topics, from lifestyle and travel to everyday inspiration, making his work relatable to a broad audience.

Outside of writing, Michael enjoys spending time outdoors, experimenting with new farming methods, and exploring different cultures through food and travel. His approachable voice and well-researched insights make his blogs both informative and engaging.